Account Aggregators Will Reshape Indian FinTech — But Many Startups Still Treat Them as Optional

FINTECH

Are you still applying for a loan and tired of uploading dozens of bank statements, tax records, and investment documents — often repeating the same process with multiple lenders? For decades, this slow, manual way of sharing financial data was the norm in India.

That’s changing with Account Aggregators (AAs): a consent-based financial data-sharing framework in which Account Aggregators are licensed by the Reserve Bank of India (RBI) as NBFC-Account Aggregators (NBFC-AAs). In simple terms, AAs help move verified financial information between regulated institutions and apps — with explicit user consent and strong security standards.

Yet, despite rapid ecosystem growth, AA integration across fintech product stacks remains uneven. Many teams still treat AAs as a “nice-to-have” instead of designing products around consented, machine-readable financial data.

What Are Account Aggregators?

Account Aggregators (AAs) are regulated intermediaries that enable individuals and businesses to share their financial information securely and with consent. Importantly, an AA is not supposed to store, process, or sell customer financial data. Instead, it acts as a consent manager and a secure relay for encrypted data flows between regulated entities.

How Do Account Aggregators Work?

1) The user gives consent to share selected financial information with a bank, lender, or fintech app (the “requesting institution”).

2) The AA sends a secure, consented request to the relevant Financial Information Provider (FIP) (for example, a bank).

3) The FIP encrypts the requested data and transmits it through the AA.

4) The AA relays the encrypted data to the Financial Information User (FIU) (the institution/app that requested it) without being able to read the payload.

5) The FIU uses the data for services such as underwriting, credit assessment, or personal finance insights.

Consent can be revoked at any time. Revocation prevents future data pulls under that consent; it does not automatically “erase” data already received by an FIU (retention is governed by the FIU’s policies, consent terms, and applicable law).

Why India’s AA Framework Is Considered a Game Changer

Users control their financial information through explicit, granular consent — aligned with the DPDP framework’s emphasis on informed, purpose-limited processing. Consent can be time-bound and revocable, and withdrawal prevents future data pulls under that consent (note: any data already received by the FIU is governed by its retention, audit, and deletion obligations).

AAs can reduce paperwork and turnaround time by enabling digital, verified data sharing (especially for lending and onboarding).

Data transmitted through the AA framework is encrypted end-to-end, and AAs are designed to relay data without reading or storing customer financial information. In a DPDP era, teams should pair AA flows with strong safeguards — access controls, logging, anomaly detection, and a clear breach-response playbook — because responsibility doesn’t end at consent.

AAs are licensed and supervised by the RBI as NBFC-AAs, with defined operational, consent, and security requirements. DPDP adds a horizontal privacy layer for all digital personal data processing, so FIUs/FIPs must also meet DPDP duties (clear notice, purpose limitation, data minimisation, retention/deletion, and grievance redressal) even when AA is the data rail.

Practical takeaway: AAs remain valid — and arguably more valuable — post‑DPDP because they create standardised, auditable consent artefacts. But AA compliance is not the same as DPDP compliance: product teams still need DPDP‑grade notices, retention controls, and security governance across the full data lifecycle.

What Real Adoption Looks Like in India Today

India’s AA network has moved well beyond pilots. As of September 2025, Government of India updates reported:

• 112.34 million users had linked their accounts in the AA ecosystem.

• Over 2.2 billion financial accounts were enabled for consent-based sharing through the AA framework.

• 112 financial institutions were live as both FIPs and FIUs (with additional institutions live as only FIP or only FIU).

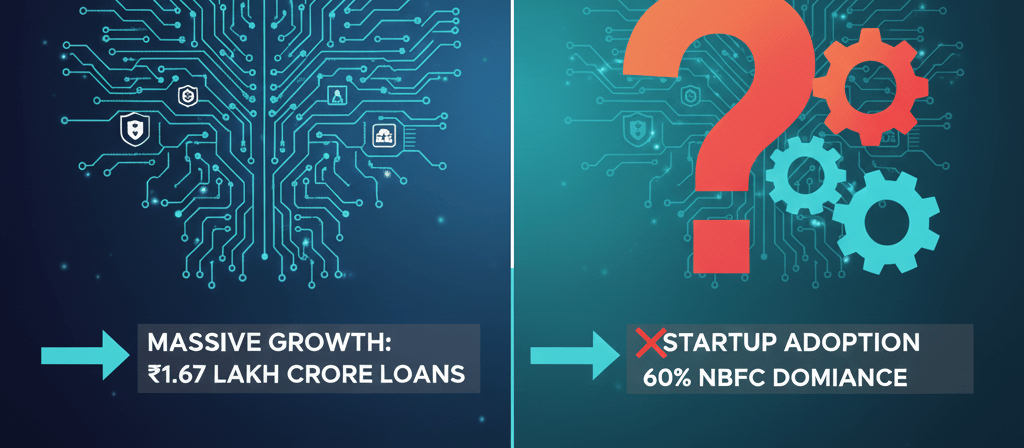

In lending specifically, an impact report by Sahamati estimated AA-enabled disbursements of about ₹1.67 lakh crore in FY 2024–25 across roughly 189 lakh (1.89 crore) loans (based on reported data from participating lenders).

Because of this trajectory, AAs are often described as a “UPI-like” layer for consented financial data sharing — an infrastructure primitive for open finance.

Where AAs Are Already Making an Impact

Lending and credit approvals: verified, directly-sourced data can reduce manual document collection and lower the risk of tampered statements, improving underwriting speed and quality.

Wealth and personal finance: as more institutions connect, AAs can support account aggregation for personal finance management, assisted advisory, and portfolio visibility (depending on which data types and FIPs are live).

Why Adoption Still Feels Slow Inside Many Startups

Integration and coverage variance: the practical usefulness of AAs depends on whether the relevant FIPs are live for the exact data needed. Coverage and data richness can vary by institution and product type.

UX and consent flows: consent journeys add steps, and weak UX can reduce completion rates. Startups need careful design to make AA flows feel seamless.

Security and fraud pressure: the ecosystem has faced fraud attempts, and some AA apps have temporarily restricted certain features in response — increasing perceived friction.

Short-term ROI bias: many early-stage teams prioritise faster-to-launch revenue levers (payments, marketplaces, embedded credit) and postpone deeper AA-based data infrastructure work.

What Needs to Change for Wider Adoption

Richer and more consistent data coverage (including deeper transaction and liability data where applicable), plus continued onboarding of more FIPs and FIUs.

Clearer, proven business cases beyond onboarding — for example, better risk models, lower fraud, improved collections, or higher approval rates.

More ecosystem education: product teams need to understand how AA-based data can reduce operational costs and improve user trust when designed well.

The Road Ahead: From Feature to Infrastructure

India’s Account Aggregator framework is more than a buzzword — it’s foundational plumbing for open, secure, consent-based financial data sharing. The question for fintech builders is no longer whether AAs matter, but whether their products are being designed to fully leverage consented, verifiable data as a core input.